Business Loan Without Documents

If you have been searching for a business loan without documents, you are probably looking for one of two things:

- Either you need funds urgently and do not want to spend days preparing paperwork, or;

- You suspect your bank statements and financials may not be strong enough to support a traditional credit application.

The first thing to know is this: it is not common for banks or financial institutions in Singapore to offer a business loan with absolutely no checks at all.

In a normal SME loan application, lenders usually review the business’s latest 6 months operating bank statements and, in some cases, financial statements as part of their credit assessment.

Your business and individual credit profile also matter.

That said, there are indeed business loans marketed as “no documents required” or close to it.

There are business loan products without documents required. But it does not mean guaranteed approval, or no credit underwriting.

It simply means the bank may not require you to manually submit documents in the traditional sense. The credit assessment still happens in a more digital and backend-driven way.

What does “business loan without documents” really mean?

In practice, a no-document business loan usually means no manual document submission rather than no due diligence.

Usually for loan applications, a bank may request for documents such as:

-

Latest 6 months bank statements

-

Latest financial statements

-

Directors’ particulars

-

Notice of Assessment or income-related information for the business owner/personal guarantor

With a digital application flow, some of this information can be pulled or verified electronically after you give consent during the online application.

Myinfo Business is specifically designed to let businesses share corporate and applicant data for simpler online transactions, with less form-filling and a reduced need for supporting documents.

Singapore’s Singpass/Myinfo ecosystem is also designed to reduce document uploads by retrieving verified data from government sources.

That is why some products can be described as “no documents required” even though the bank is still assessing plenty of data points behind the scenes.

Why most business loans still require documents

For most SME loans, lenders still want to see how the business is actually operating. One of the most common way banks assess cash flow is the business's latest 6 months operating bank statements. These help the lender assess whether:

-

The business has regular incoming payments

-

Cash floats are healthy or constantly stretched

-

There are returned cheques/Giro or adverse account conduct

-

The business can service debit commitments

This is exactly why traditional loan applications are usually more documentation-heavy.

If you are not familiar with how banks look at bank statements, our guide on 6 Ways To Improve Your SME Loan Approval Chances is a useful read.

In other words, when a lender does not ask you to submit bank statements, it still needs other reliable ways to assess the risk.

How does a “no document” loan still work?

A lender cannot lend blindly. If it is not relying on bank statements or financial statements, it has to lean more on other data points that can be obtained digitally or through backend searches.

1. The business itself is still assessed

Even in a no-document paperless application, the lender will still assess the borrowing entity. Typical factors and data points that can be credit-assessed may include:

-

Age of business

-

Business industry

-

Company structure

-

Paid-up capital

-

Number of directors and shareholders and appointed dates

-

Company profile, regulatory and compliance filing history

This is one reason why newer businesses, businesses in higher-risk sectors, or companies with more complex shareholding structures may not always qualify for the simplest digital loan journeys.

Your broader credit eligibility across banks can also vary significantly, which is why many SMEs start with a comparison approach such as our Business Loan Compare page.

2. The business owner is a major part of the assessment

For unsecured SME financing, the business owner is very often a personal guarantor. If the bank is not reviewing full business documents, then the guarantor’s personal profile bears an even higher weightage in credit assessment.

This usually includes checks such as:

-

Personal credit bureau profile and repayment conduct

-

Existing outstanding credit facilities

-

Gearing and leverage

-

Income reported in the owner’s NOA

-

Whether there are any adverse credit events

-

Debt servicing behavior/repayment conduct on personal credit facilities

Business owners often underestimate how much their own credit conduct can influence SME borrowing outcomes.

3. Digital consent replaces manual paperwork

When you apply online, you may be asked to authenticate via Singpass or Corppass and give consent for the lender to retrieve or verify relevant data.

Myinfo Business says businesses can share both corporate and applicant personal data for simpler online transactions. That is why the product can honestly be marketed as “no documents required” from the borrower’s point of view.

So the phrase business loan without documents should really be understood as business loan without manual document submission.

Banks with no documents business loan

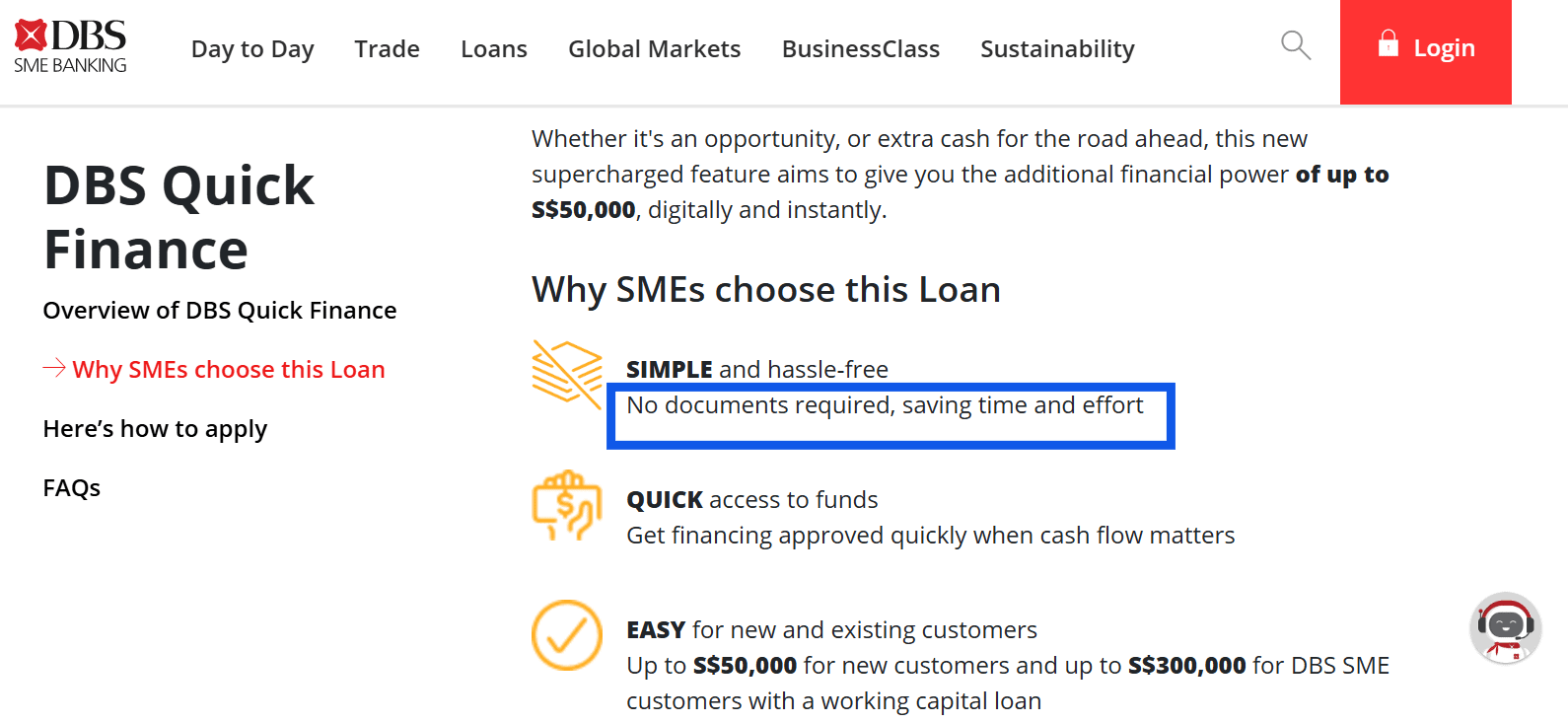

DBS Quick Finance: New to DBS customers can access up to S$50,000 with no documents required.

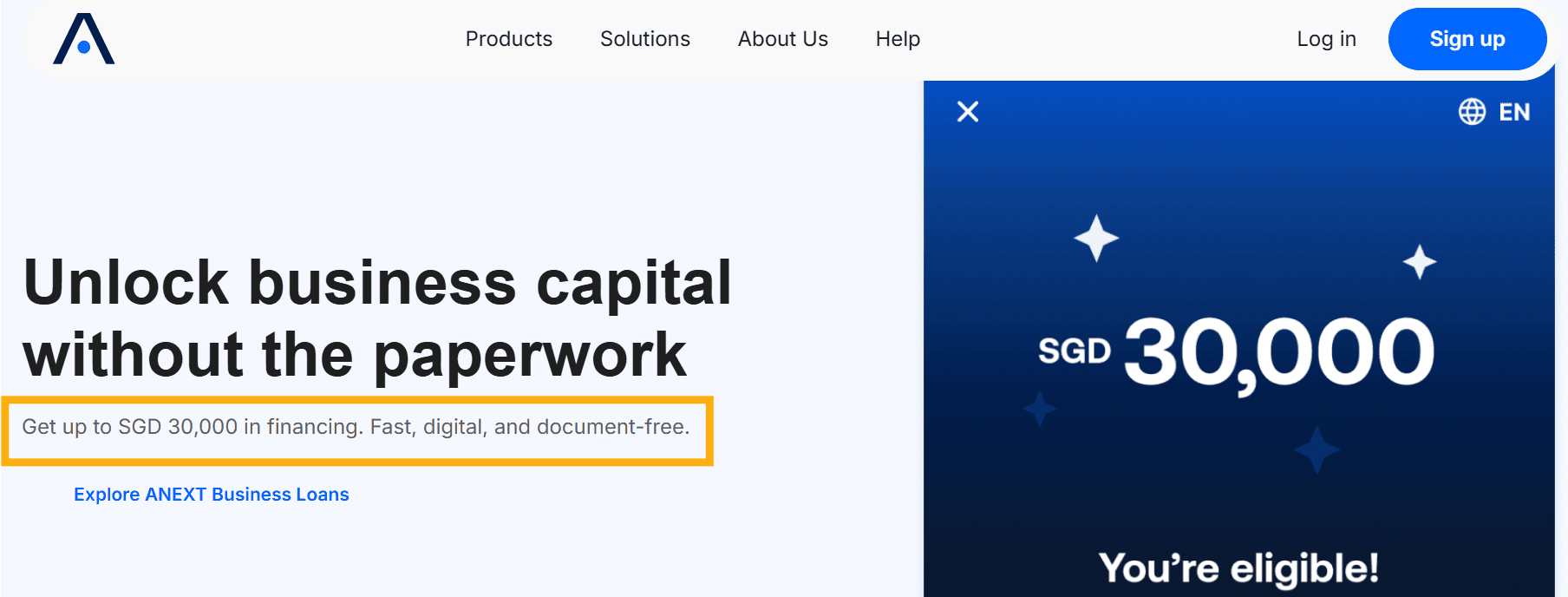

Anext Business Loan ; Offers up to $30,000 with no documents required.

* Above listed bank products accurate at the time of writing. Banks' products are subject to changes, please do your own research or engage a professional financing consultant to advise.

Pros of a business loan without documents

Faster turnaround

Because there is less manual paperwork and back-and-forth, underwriting can often move faster. For SMEs facing time-sensitive working capital needs, speed matters.

Less admin work

SME owners are busy. A digital, paperless application is far more convenient than hunting down statements, accounts, and corporate documents.

Useful for smaller urgent cash flow needs

If the business only needs a smaller loan amount to bridge a short-term cash flow gap, a no-document loan can be practical.

Full documents may not present strongly

Some businesses are viable and operating, but their latest bank statements may be messy, volatile, or seasonally weak.

In such situations, a smaller-ticket digital loan assessed with a wider mix of data points may sometimes be a more realistic starting point than a full traditional loan application.

Cons of a business loan without documents

Loan quantum is usually smaller

The less information a lender reviews, the more conservative it is likely to underwrite. In practice, many no-document loans tend to be smaller-ticket.

A rough real-world expectation for many SMEs may be somewhere around S$10,000 to S$30,000, rather than six-figure facility.

Pricing may be higher

When the lender takes more risk uncertainty and handles a smaller loan ticket, pricing may not be as attractive as a conventional business term loan backed by full documentations.

SMEs should always look beyond the headline rate and factor in processing fees and redemption penalties as well.

It is not “sure approved”

This is a big misconception. No documents does not mean guaranteed approval. The lender is still assessing creditworthiness. It is simply using digitally retrieved data, backend searches, and credit scoring rather than relying only on uploaded documents.

Personal credit matter even more

If the lender is not relying as much documentations of the business, the owner-guarantor’s credit profile will become even more important.

That is especially relevant for sole proprietors and smaller owner-managed businesses.

Machine based algorithms leave no room for mitigations

For such no-documents loans, the credit underwriting process most definitely is algorithm driven, based on a pre-defined set of credit parameters set up by the banks.

In such algorithmic loan applications, applicant either gets a Yes/No answer, usually within minutes or same-day. This leaves no room for mitigation or explanation, if the business profile does not tick all boxes.

Full-documents traditional loan applications may still allow some flexibility and manual intervention to justify and mitigate certain credit concerns.

Who should consider a no-document business loan?

A business loan without documents may be worth considering if:

-

You need funds urgently

-

Loan amount needed is small (less than $30K)

-

Your personal credit profile is very healthy

-

You just need a short-term buffer rather than a large structured facility

When a normal full-document business loan may be better

A traditional business loan application with full documentations may be better if you:

-

Need a larger loan quantum (more than $50K)

-

Can present decent bank statements

-

Want access to more lenders and more loan structures

-

Want a better chance of securing lower rate and higher approval odds

-

Case benefits from proper representation and credit packaging

In those situations, it may be better to submit a full documents credit assessment rather than avoid it.

A stronger set of documents can unlock better rates, higher approval chances, and larger quantum.

Final thoughts

A business loan without documents is real, but it is the exception rather than the norm.

In Singapore, most banks and financial institutions still prefer to assess a business using bank statements, financial information, and the owner-guarantor’s credit profile.

However, some products can offer a paperless borrowing journey by retrieving and verifying data digitally instead of asking you to upload documents manually.

The important thing to remember is that no documents does not mean no underwriting. It also does not mean guaranteed approval.

What it usually means is this: the bank is still assessing risk, but it is doing so through backend data retrieval, credit searches, business-profile checks, and digital verification instead of a traditional stack of paperwork.

If you are exploring this route, the smarter question is not just “Which bank gives a business loan without documents?” The better question is: Which lender is most likely to approve my business based on the data they can see?

Compare your best business loan options instantly with our online loan assessment tool.