Enterprise Financing Scheme (EFS)

The Enterprise Financing Scheme (EFS) is a scheme administered by Enterprise Singapore (ES), a statutory board under the Ministry of Trade and Industry. ES was formed after a merger of Spring Singapore and IE Singapore.

The Enterprise Financing Scheme consists of 6 separate government assisted financing schemes that is grouped under one umbrella, EFS. These financing schemes are supported by various participating financial institutions (PFIs).

Applications for the schemes are assessed and underwritten by these PFIs. ES will share the loan default risk together with the PFIs.

The EFS aims to provide targeted financing instruments to better support Singapore SMEs throughout their various phases of growth. We’ll go through the 6 different schemes under EFS and whom they are relevant for.

SME Working Capital Loan

The SME Working Capital Loan is a unsecured term loan to finance day to day general cash flow requirements.

The maximum loan amount is $300K per borrower. Maximum limit will be increased to $500K from October 2022 to March 2023.

The maximum repayment period is 5 years. There are close to 20 banks and financial institutions participating in this scheme. Interest rate and credit criteria differs for each financier and are subject to respective participating financial institutions' credit risk assessment.

SME Fixed Assets Loan

This facility provides businesses financing for the purchase of local or overseas fixed assets such as equipment and machinery. Construction and development costs of factories and business premises is also covered under this loan.

- Maximum loan quantum S$30M

- Maximum repayment period 15 years

- Up to 50% risk sharing, up to 70% for young enterprises

Such equipment and machinery loan financing is suitable for companies looking to invest in specialized, high tech or customized equipment/machinery that improves operational productivity. The high capex incurred for such purchases can be financed under this scheme.

Venture Debt Loan

Loan for innovative and high growth startups, structured with Venture Debts and Warrants, like a hybrid between debt and equity financing.

With a maximum loan quantum of up to $5M, this scheme is tailored for high growth startups that might not qualify for traditional startup business loan from mainstream banks. Venture loans are typically suitable for startups that do not necessarily have positive cashflow or hard assets to use as collateral.

Trade Loan

Trade financing facility to finance import, exports and general trading requirements. This covers essentially the below business activities:

- Import of inventory / stock financing

- Structured pre-delivery working capital (revolving working capital)

- Factoring (with recourse) / bill of invoice / AR discounting

- Local and overseas working capital and trading transactions

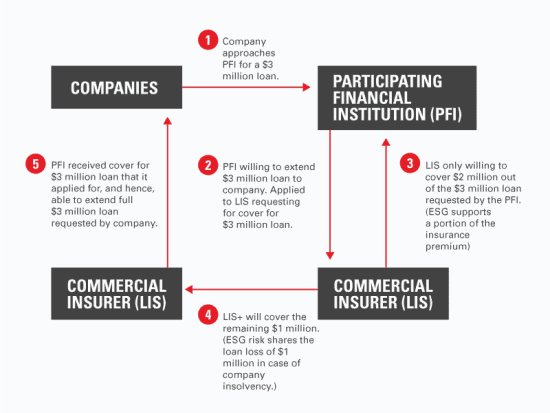

The Loan Insurance Scheme (LIS+) under the Trade Loan also serves as a complement and additional support for commercial trade financing insurers whom might not be able to provide full coverage on approved credit limits.

Project Loan

This loan is primarily targeted to help companies finance overseas projects secured. Aside from working capital loan, funding can also be tapped for financing of fixed assets deployed for the project, such as equipment and machinery.

Combination of trade financing and working capital financing can also be utilized, with a maximum loan quantum of up to $50M under the Project Loan.

Mergers and Acquisition Loan

For mature and larger SMEs and businesses looking to acquire a local or overseas enterprise, the M&A loan could be tapped on for acquisition financing.

The end goal and purpose of the merger and acquisition should be with the intent of internationalization. Maximum loan quantum of $50M is applicable for this loan scheme.

Government financing schemes

Running a SME in Singapore is challenging. High rental costs, tight labor market and tough access to bank financing are some of the pertinent challenges most SME owners face when trying to scale their operations.

Singapore is already one of the most expensive city in the world to conduct business in and local SMEs constantly have to grabble with high overheads and costs. Fortunately, there are a myriad of grants and financing schemes SMEs can tap into to help alleviate working capital and cash flow pressure.

SMEs made up 99% of all enterprises in Singapore, contributing almost 50% of GDP and employs about 70% of the workforce. Due to lack of resources, information and time, most small business owners might not be aware of the various grants and financing schemes SMEs can tap into.

Most government assisted financing schemes for SMEs are administered by Enterprise Singapore, a combined entity that after the merger of Spring Singapore and IE Singapore, to champion the growth of SMEs.

Most financing schemes such as the Temporary Bridging Loan, have some form of risk sharing between the government and participating financial institutions. This help encourage banks and financial institutions to spur credit lending to SMEs which are traditionally considered high risk segment to banks due to lack of credit information and higher default rates.

Securing a business loan in Singapore is no easy feat for most SMEs and such financing schemes definitely help to improve approval chances.

With the risk sharing element from the government, banks participating in these schemes might also offer lower interest rates on a SME loan since the risk of default is now co-shared.

These government financing schemes also help as a stabilizer to improve funding liquidity in the banking credit ecosystem as most banks will generally slow down lending to mitigate risks during a economic downturn.

With the engines of funding access being throttled, SMEs will face a double whammy with declining revenue and working capital squeeze during economy slowdowns. The government funding schemes therefore aims to encourage bank lending and lower financing costs for SMEs.

There are close to 20 banks and financial institutions participating in some of the government aided financing schemes. Every bank and financial institution have their own credit risk assessment, business loan interest rate and criteria which might vary.

SMEs are encouraged to do their own research or engage competent financing consultants to find out which schemes are suitable for their requirements.