Credit Bureau Report And Credit Rating Affects Business Loan

Table of Contents

Your personal credit rating reflected in your credit bureau report affects your ability to apply for consumer and business loans. This include credit cards, car loan, home loan and SME loans.

Bank loan for business applications in Singapore are also subjected to the business owner’s personal credit score. We have encountered countless business loan applications that were rejected due to poor personal credit rating of the business owner.

Some of these businesses have very good bankable profile and would have easily qualified for a business loan; alas rejected due to the owner’s poor credit grade.

A decent credit score is essential for qualifying for a business loan from a bank or financial institution. Some business owners don’t think much about their credit score, especially when they don’t have an immediate financing need.

Before you apply for a business loan, it would be prudent to check out your credit score.

What is a credit bureau report?

You can access your credit score and grading by purchasing your credit report from Credit Bureau Singapore (CBS) for $8 (before GST). If you’ve recently applied for a credit facility from a bank, you might be able to obtain a free credit report within 30 days.

CBS is a collaborative effort between the Association of Banks in Singapore and Infocredit Holdings. It is Singapore’s primary credit bureau, established to collect, manage, and share credit-related data among financial institutions.

Your CBS report reflects your current and past credit facilities, repayment conduct of these credit facilities, and most importantly your credit score and grade.

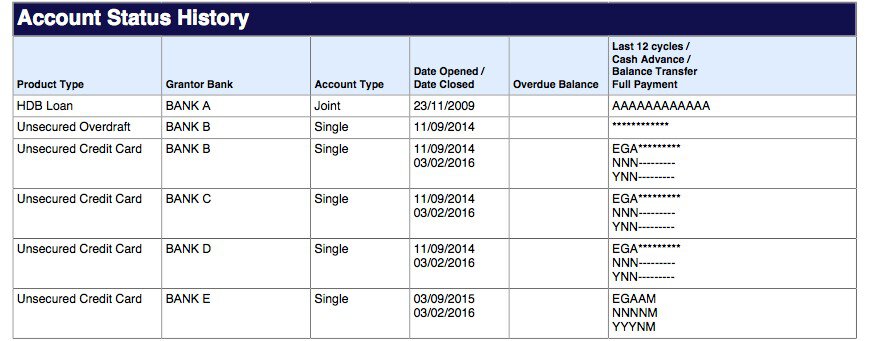

From the above sample extract, the account status history of the credit report forms a critical part of your credit profile. It details the current and past personal credit facilities you hold, and most importantly, your payment conduct over the last 12 months cycle.

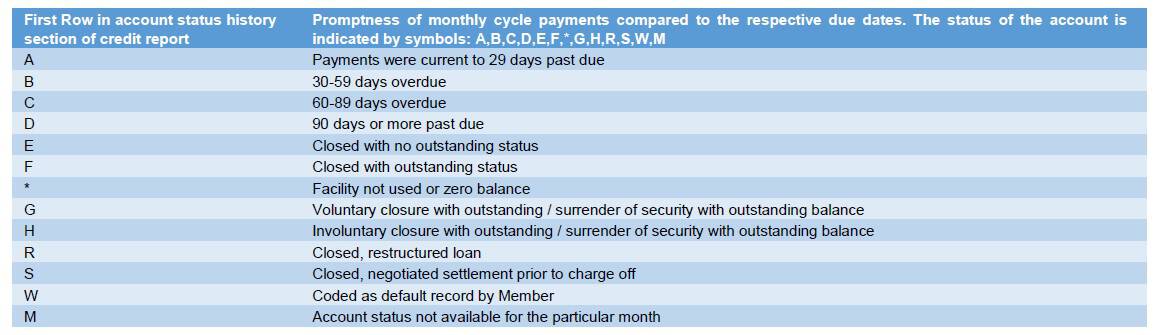

In the top row of each credit facility, your latest repayment records are displayed with the most recent month on the most left. What you should be looking out for is the status ‘A’ as it denotes that payments are current to 29 days past due. Below is the full legend of the ageing status.

Credit score and grade

The repayment conduct information in your credit file will be used to generate a credit score and risk grade by CBS using advanced modelling and analytics.

The CBS Credit Score ranges from 1000 to 2000. This score is correspondingly tagged to risk grades between AA (best) to HH (worst). Banks may use this score and grade to predict an individual's likelihood of future repayment performance and risk of default.

What is a good credit score?

From our professional experience, in the context of SME financing, banks usually use the CBS risk grade (AA to HH) more so than the credit score (1000 to 2000) to set minimum benchmarks and inform overall credit assessment.

A good credit grade score is between AA to BB. Credit grade between CC to EE would be deemed somewhat average. Credit grade from FF to HH are the weakest grades from a credit perspective.

The business owner’s risk grade is a vital component of a business loan assessment, but not the only one. Banks assess a credit application based on a totality case-to-case basis.

There are many more credit factors aside from CBS score that determines whether an application will be successful approved.

What does a credit rating score of HH mean?

A credit rating of "HH" indicates the lowest and worst scored risk grade on the CBS scorecard, placing an individual in a category with lower creditworthiness. Individuals with a grade of "HH" typically have an elevated probability of default and may face challenges when applying for credit.

It is important to note that your credit score is an objective number determined by CBS independently based on the information in your CBS report. It is optional for banks to use this credit score in their internal credit assessment. CBS is not involved in the credit lending decision of banks.

Minimum credit score for business loan

There is no prescribed industry standard minimum credit score to qualify for a business loan. As discussed above, the business owner’s credit score is just a single component of a bank’s credit assessment matrix, albeit a very important one.

From thousands of cases we’ve consulted with since 2012, business owners with an HH credit grade typically have the lowest chance of securing financing. GG risk grade would seem to be the minimum credit score for business loan.

But it is not a certainty business owners with HH credit grade can’t secure financing. We have secured approvals for HH risk grade cases before, if we can justify to banks’ credit underwriters the HH grade is not due to borrower’s credit unworthiness, but due to other reasons.

Examples include disputed credit card annual fees, or purchasing a new home thus enquiring with multiple banks for lowest rate home loan packages etc. (multiple applications in a short period will impact credit score).

There are many nuances to this. Business owners with AA CBS grade could still have their business loan applications rejected, if the business does not fulfil other credit criteria of banks. An example would be the BTI ratio requirement.

Balance to Income (BTI) ratio

This is a borrowing limit imposed by MAS for all individual borrowers. BTI ratio is calculated by dividing your total unsecured interest-bearing outstanding balances across all financing institutions, by your monthly income.

MAS imposes a maximum BTI ratio of 12 times as an industry wide borrowing limit. Financial institutions will not be able to grant further unsecured credit limit to individuals whose BTI exceeds 12 times of monthly income for three consecutive months.

For SME business loans, there’s no specific regulatory cap on business owners’ BTI ratio

In practice, most banks will raise concerns or even restrict business lending if the business owner’s BTI ratio exceeds 12 times. This applies even if he/she has a good CBS grade of AA or BB. (Yes, individuals with high BTI ratio can still score a AA or BB risk grade if there's a long history of prompt repayment conduct).

A high BTI ratio indicates indebtedness of an individual who might be struggling with excessive leverage.

You can check your total unsecured interest-bearing balances in your CBS report.

We advise business owners who are financing their business with personal loans to shift their debt commitments to business loans instead.

This helps reduce their personal BTI ratio and avoid getting into a tight spot on personal credit restrictions.

Non-scored risk grade

Some individuals might not see any credit score in their CBS report. No credit score is accorded if you have a very short credit history, no credit facilities or minimal facilities without recent updates.

This is the case as well for individuals with a prior public record ((i.e. litigation proceedings/bankruptcy records) or a current severe default record.

For those without a credit score, a “Not Applicable” remark will be shown, and a non-scored risk grade will be assigned.

Let’s look at some common examples of non-scored risk grades.

What does credit bureau score GX mean?

A "GX" score indicates that the CBS report contains only inquiry records without any associated credit activity or defaults. This score is commonly assigned to those without active credit facilities or who only make self-enquiries or inquiries by financial institutions for background checks. The "GX" grade often means that credit assessment is challenging due to a lack of detailed credit history.

Risk grade CX credit rating

The CX rating is a non-scored risk grade that reflects insufficient credit activity or data. This grade usually applies to individuals with minimal or no credit history, making it difficult for CBS to calculate a credit score.

Since this score indicates limited credit exposure, obtaining a loan could be challenging, as financial institutions rely on credit history for underwriting.

Both GX and CX risk grade are for individuals with no or minimal active live personal credit facilities. Some business owners have a misconception that no active credit facilities equates to a good credit profile. “I don’t owe any banks and I pay everything in full cash.” is a common refrain. This is far from the truth and some banks will reject GX and CX risk grades cases outright. You’ll need active credit facilities so banks can have a measure of your repayment conduct and creditworthiness.

HX and HZ credit rating

HX is a non-scored risk grade accorded if you have existing or a past Writ of Summons, Bankruptcy Petition or Bankruptcy Order record filed.

HZ risk grade: Credit facilities that are currently more than 90 days past due / write off with outstanding balance ≥ $300.

Both HZ and HZ grades are adversely damaging to a business loan’s approval chances. Virtually all doors are shut for HZ grade, since it’s a default record.

For HX grade, if the business owner can provide documentations proving litigation issues have been resolved, and if current personal credit facilities reflect good repayment conduct, the case can still be mitigated.

Else, if the adverse litigation against the business owner is due to common and minor traffic accidents cases, generally no issues as well.

How to get a business loan with no credit?

It is more challenging to secure a business loan if the business owner has no active credit score (i.e. CX or GX). Contrary to popular belief, an individual with no loans and liability is not deemed a good quality borrower.

It is not impossible to secure business financing with no credit grade. Loan amounts will be smaller for a start.

If you have loans that are not reflected in Credit Bureau's credit report, submitting the last 12 months repayment records of such loans might help improve approval chances. Such loans include HDB loans or car loans with non-bank leasing/financing lenders.

To get a business loan with no credit, you should start obtaining banks' credit cards. Put spend on these cards, and ensure full repayment before statement due date. Your credit score will improve, putting you in a better position to secure business loans.

Can I get a business loan with bad credit?

Again, this depends as every case is unique. Plenty of nuances and details to this question. If there are existing defaults records with outstanding amounts, or if payment conduct for multiple existing facilities are very tardy, it’s likely a no-go.

However, there’s a broad grey area in between, where it really depends on a case-by-case basis. If there’s a reasonable justification or explanation for certain deficiencies in credit score, mitigations can be put up for an appeal.

Different banks and lenders might have varying opinion on what exactly constitutes “bad credit”. Non-bank alternative financiers might be more lenient for minor credit misconduct, as their higher interest rates could compensate for higher risk undertaken.

What impacts credit score?

- Credit Repayment History: Late payments and the lack of a consistent record of on-time payments will adversely impact credit score.

- High Credit Utilization: Utilizing a high percentage of total available credit limits suggests potential over-reliance on credit.

- Frequent Credit Applications: A high number of credit inquiries triggered by multiple loan applications within a short span of time will affect credit score. A high number of inquiries by lenders can be seen as a sign of financial distress

- Short Credit History: A limited credit record may contribute to credit risk uncertainty, and hinder credit score calculations.

- Increasing Debt Exposure: High, unpaid outstanding balances that is trending up over the recent few months will result on a hit in credit score.

- Adverse credit history: A history of negative credit events, such as defaults or bankruptcies, is a strong indicator of higher credit risk and can severely damage a credit score

Credit card annual fees

A frequently encountered cause of low credit score is unpaid credit card annual fees.

It is a common practice amongst most of us to seek bank’s waiver of credit card annual fees. Some do not pay the fee if waiver request is rejected, thinking it’s not a big issue and they’ll just cancel the card.

If one were to leave this issue unattended, the unpaid annual fee, if not waived by the banks, continues to attract late fees and interest, which keeps snowballing. Amount is not large, but the negative impact on your credit score is outsized. This will be recorded in CBS as a perpetual late payment.

If the bank eventually relents and writes off internally the annual fee and late fees, they might close the card and lodge a H status in CBS. H payment ageing status is “Involuntary closure with outstanding”. This is akin to a sledgehammer blow to your credit score.

Our suggestion is to pay the annual fee first, then seek waiver from the bank. If the fee is waived, it’ll be reversed in subsequent month’s statement.

If not, it’s usually just a small sum, but the price of an adverse hit to your credit score could be heavy. Especially so if you just happen to require financing for your business.

Does personal self-enquiry on your credit report impact your credit score?

There’s a common misconception that purchasing your credit report by running a self enquiry will result in a credit score drop.

This misconception stems from the fact that multiple enquiries by banks when assessing new credit applications does indeed affect your credit score.

When you purchase your own credit report, the product type reflected will be “Self”

Such self enquiries do not affect your credit score at all as it’s not for the purpose of a new credit application. This fact has also been shared directly by Credit Bureau in a Straits Times forum on September 2023.

“Likewise, review inquiries conducted by CBS members, under ongoing monitoring checks on their customers with existing loan facilities, and consumers retrieving their own credit reports have no impact on the credit score.”

Lily Tay

Business Development Director

Credit Bureau Singapore

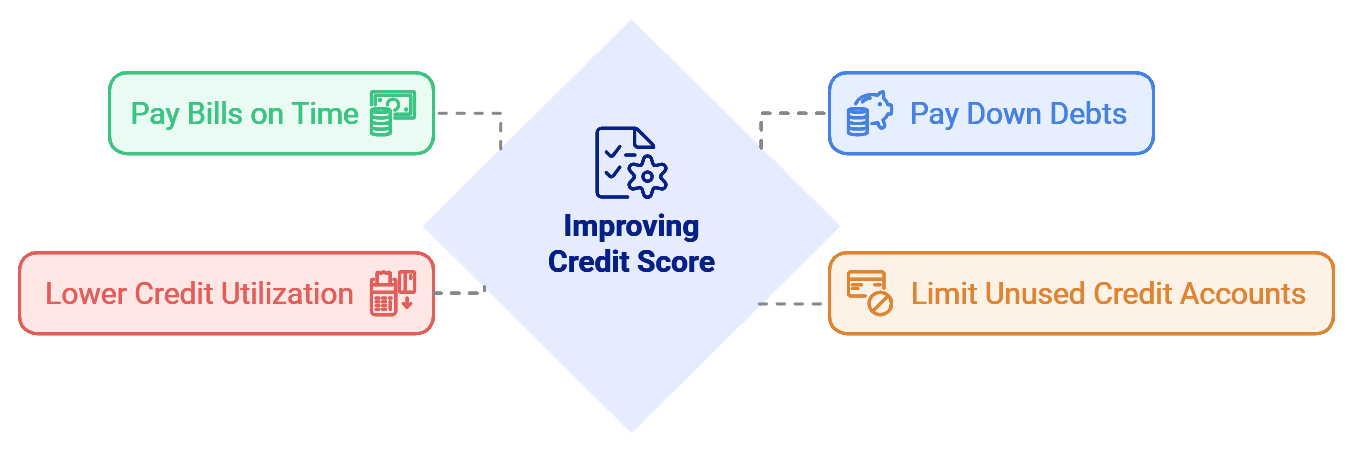

How to improve credit score and rating?

Pay bills in full and on time: Timely consistent full payments demonstrate responsible credit management and build a strong credit history. If you can’t pay it off all at once, make sure you at least pay the minimum amount billed every month before the due date.

Pay down debts as quickly as possible: Reducing outstanding debt, especially for credit card rollover outstanding balances, will minimize interest charges and reduces the credit utilization ratio which positively impact the credit score.

Limit unused credit accounts and limits: Cancel inactive credit cards. If you have very high credit limits on your cards, request your banks to lower the credit limit of your cards. High aggregated credit limits from unsecured credit facilities will impact your credit score even if you don’t draw down on the limits.

Lowering Credit Utilization: Using less than 30% of available credit is advisable. Avoid nothing more than 70% utilization at most.

Other practical tips from our experience

We do understand situations when there’s a cash flow crunch and it’s just not possible to make full payments on all credit card bills.

To protect your credit score from further deterioration, the next best thing to do is to pay off credit cards with smaller outstanding amounts first in full.

For example, if you have five credit cards with $10K each in outstanding balances, totalling $50K, and you’ve only $30K available for payment. Instead of paying each credit card $6K, you should pay 3 credit cards in full with $30K. Just make minimum payments on the 2 remaining cards.

You rather have 3 credit cards reflecting full payments and 2 without in your CBS report, than to have all 5 cards without full payment records.

Identity theft and credit fraud: Due to the prevalence of smartphones and ease of mobile first digital banking, identity theft and credit fraud is an emerging scourge affecting all individuals and businesses. We suggest taking proactive steps to monitor and protect yourself against identity theft.

Monitor your credit bureau records at least once to twice a year and look out for any irregular credit facilities you did not sign up for. Consider using a VPN for phone when you're overseas and need to access internet banking. Always verify directly with your suppliers or vendors if you received emails from them stating a change of payment account.

CX and GX CBS grade

If you do not have any personal live credit facilities, apply for at least one credit card. Start charging small amounts to this credit card, and make sure to pay off the statement in full every month before due date.

By doing this, you should start seeing a scored risk grade that will improve gradually within next 4 to 8 months.

If your latest reported annual income is below most banks’ minimum requirement of $18K to qualify for a credit card, try to search online for credit cards with no minimum income requirements. Such cards usually have a small credit limit of $500, but it’ll suffice to help build up your credit score.

If that’s not possible, alternatively search for secured credit cards. Some banks offer credit cards secured to fixed deposit of $10K pledged.

BTI ratio burst and exceeded

Try not to take up further personal loans and pay down all unsecured loans and credit cards outstanding gradually. When your total unsecured interest-bearing outstanding balance drops below your latest annual income reported in your IRAS NOA (Notice of Assessment), you can start exploring financing options again.

We suggest to try bringing down your outstanding balances to below 50% of your reported annual income to stand a higher chance of business financing approvals.

CBS HH grade

There are few possible reasons for this, you need to identify which one, or it could be combination of more than one reason.

Multiple new credit applications – Stop applying for new credit facilities and let your credit score recover. This will usually take between 1 to 3 months.

Unsecured outstanding balances increasing trend – Similar to the BTI ratio exceeded advice above, try your best to pay down your outstanding balances below your annual income reported.

Late payments – Look at the top row of your current credit facilities. If you see any payment ageing status that’s not A, but Bs or Cs, there are credit facilities that were being paid later >29 days due. Make payments for these immediately and ensure prompt payments monthly. Setup Giro deductions or reminders to avoid late payments in future.

New credit facilities history - If you've just obtained your first individual credit facility within the last 12 to 16 months, your repayment conduct could be considered "fresh" and new to CBS. You might be assigned a HH grade in this case. It usually takes anywhere between 10 to 15 cycles (months) of repayment history on new credit facilities to have your credit grade move up. Continue making prompt and full repayments on your credit facility. You should start seeing improvement in your credit grade around the 12th repayment cycle.

None of the above – In certain situations, a HH risk grade could be accorded due to previous adverse credit history few years back not reflected in current CBS report. There’s nothing much you can do for this. Continue making prompt and full payments for all current credit facilities and monitor again in 4 to 6 months time.

Will taking a business loan affect my credit score?

Taking a business loan will not affect your credit score. Your CBS report will only reflect credit taken in your individual name, not loans under your business.

There is no nation-wide industry standard SME business credit bureau. The closest to that is Enterprise Singapore’s loan portal which reflects business loan taken under government financing schemes. Only participating financial institutions have access to this.

However, applying for business loans may affect your score due to credit inquiries. If you submit multiple business loan applications within a short period, it’ll result in multiple credit enquiries which could lead to a drop in your credit score.

Our modus operandi for all consulting engagements is to take a targeted approach to applications. We identify a handful of banks that we know are suitable for client’s credit profile and work on them first.

We move on to next batch of banks only if the first few ones fail to offer financing approvals. This approach minimizes CBS credit enquiries on the business owner, protecting his/her credit score.

We can do this due to our deep familiarity with every bank’s credit appetite and general criteria. This is a more prudent approach versus the “machine gun spray and pray” method, applying to every single bank in hopes of approval.

Does taking a business loan affect housing loan application?

Business owners may be concerned if a business loan might affect their mortgage application if they happen to be buying a residential property at the same time.

Residential property loans are regulated under MAS Notice 645. TDSR (total debt servicing ratio) is the industry’s housing loan calculation matrix to calculate a borrower’s monthly debt commitments.

MAS Notice 645 does not explicitly state if a Private Limited entity’s debt is included in the business owner’s commitments for TDSR calculations. If the business entity is a sole proprietorship, it’s clear that that the sole proprietorship’s debts are considered personal debts of the owner since both are legally inseparable entities.

From our observations, debt obligations of a Private Limited entity are usually not included as the business owner’s commitments for a residential property loan application in his/her individual name. Reason could be because the business owner and the business are separate legal entities.

It might be prudent though to apply your home loan with other banks that are not already financing your business. There should be less complications in this case.

Summary

Credit bureau score is one of those minor stuff some business owners do not pay much attention to but is absolutely critical when you require a business loan. A poor credit score is one of the common issues stalling loan application process.

It is a huge opportunity cost if you have to miss a business opportunity because your business loan application was declined due to poor personal credit score.

Be mindful about your credit records and consistently pay off your bills in full. This will position you in the best financing capacity when the time calls for it.