2021 SME Finance Accessibility Survey and Research

Table of Contents

Linkflow Capital operates a SME loan portal for users to compare their business financing options online instantly.

We have been aggregating data collated from our SME financing comparison platform since 2017. This report summarizes the data researched from January to December 2021.

Here’s a rundown on the statistics and sample size collated:

Total aggregated sample size of 2176 users

Duplicate and spam entries were scrubbed off database

No manual verification conducted for every user, data used "as is" provided by users

Our key takeaway from 2021’s survey data:

“60% of SMEs were ineligible for financing, a significant increase from 48% observed in 2020’s data.”

Based on our internal dataset, we opined that financing eligibility for SMEs decreased in 2021 due to:

Unwinding of various Covid-19 government relief schemes

Reduced government risk sharing for financing programmes

Changing profile of SMEs seeking financing during the height of the pandemic in 2020 versus 2021.

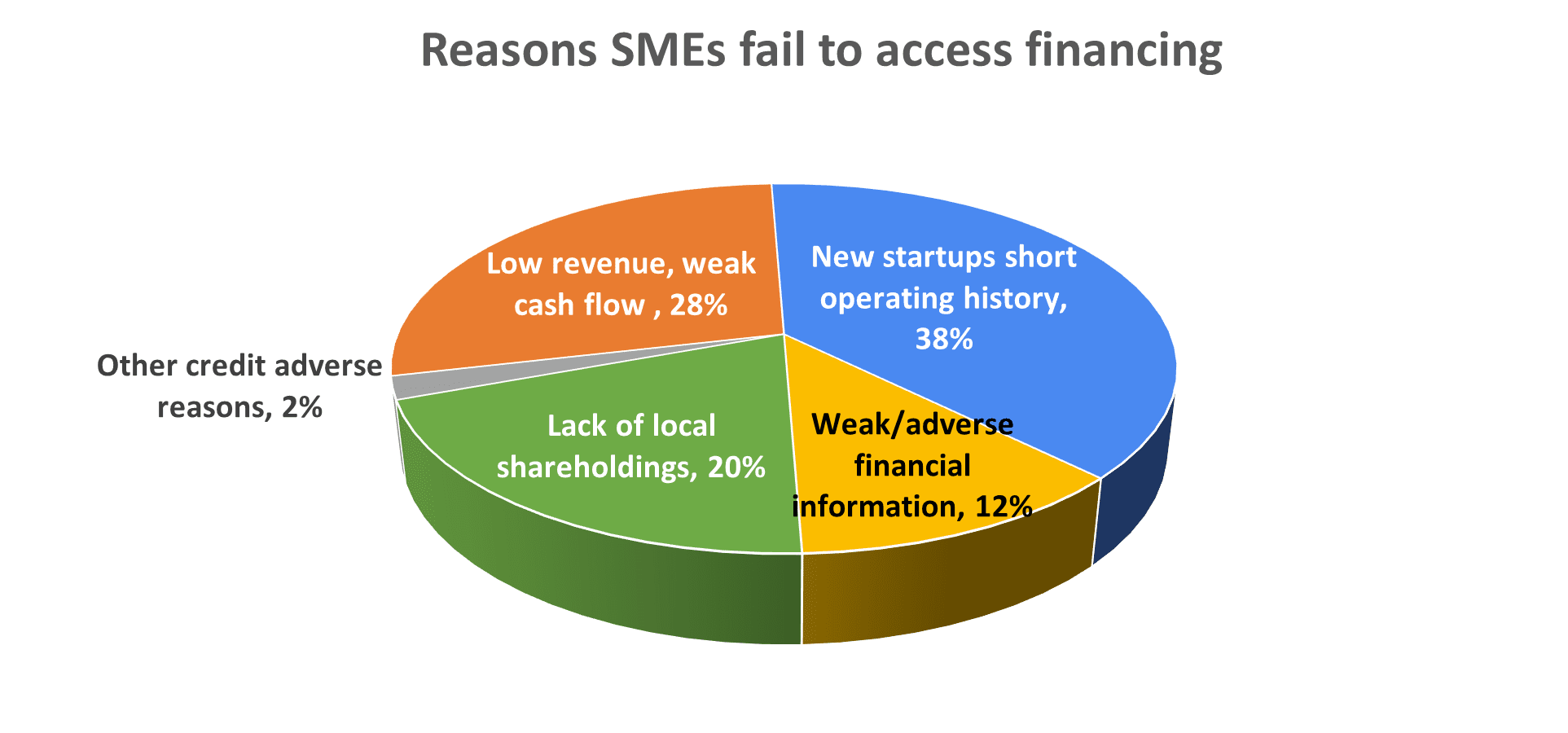

Reasons SMEs fail to access financing

For users within our platform that were unable to avail of financing in 2021, these are some of the common reasons:

38% due to newly incorporated startups with no or low revenue

28% due to smallish low revenue and weak bank balances

20% due to lack of minimum 30% local shareholdings required by most banks

12% due to weak financial performance (loss making, negative equity)

2% - Other credit adverse reasons

In 2021, for users who were not able to avail of financing, the most common reason is due to ‘new startups with short operating history’.

Most banks typically require SMEs to have minimally 1 year operating history before considering business loan applications. It is also not uncommon for some banks to require minimum of 2 to 3 years operating history.

This could be due to the higher failure rate of new startups and the inherent credit risk in financing young businesses with no viable track record.

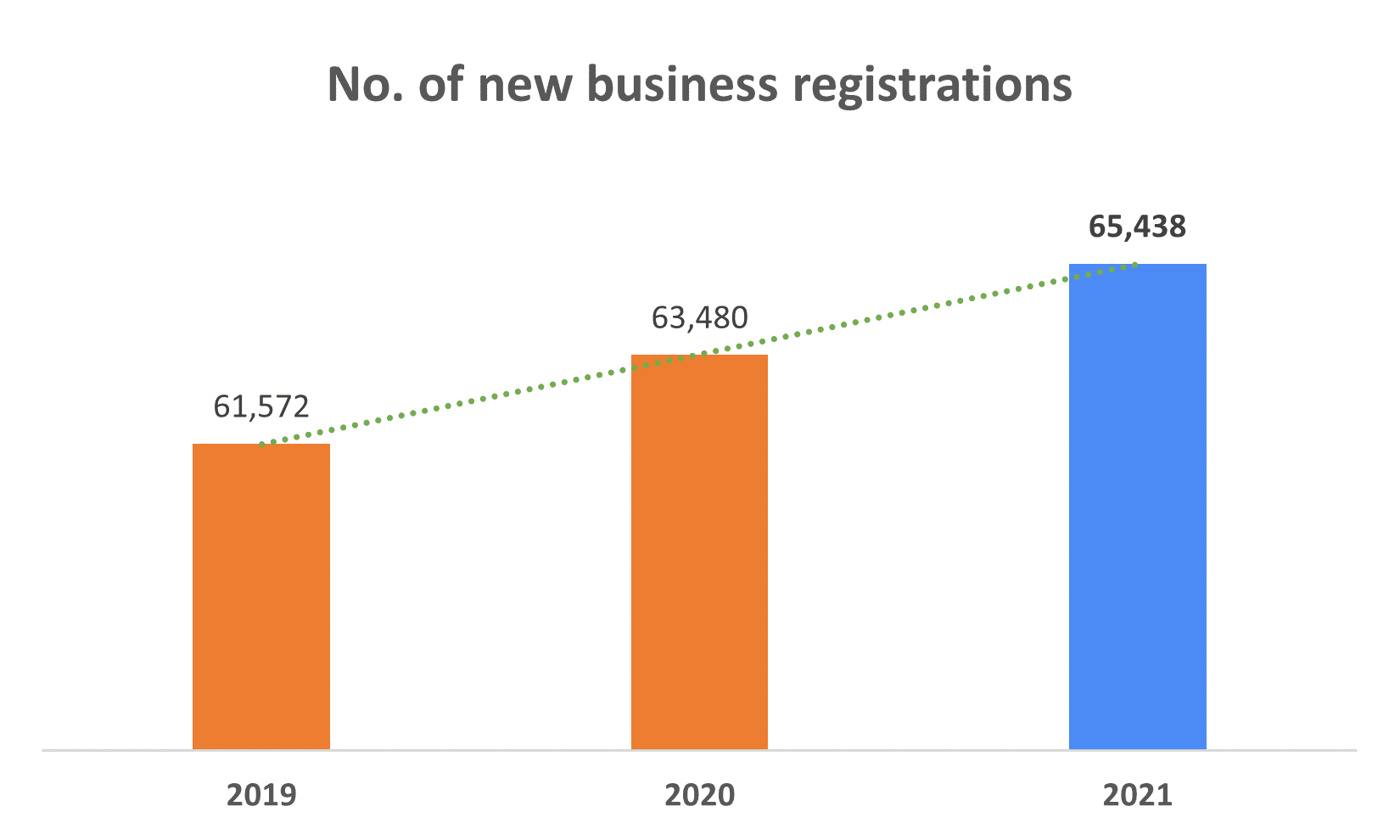

Number of new business registrations

Amongst the profile of users within our platform, the number of new startups with less than 1 year operating history seeking financing has increased steadily over the past few years.

We complied data extracted from ACRA (Accounting and Corporate Regulatory Authority) on new business formations across 2019 to 2021.

Data from ACRA [1] reflects that the number of new business registrations has grown to 65,438 in 2021, a 6% increase from 2019 pre-Covid.

The pickup in new businesses registered despite a raging global pandemic during 2020 to 2021 could explain why we are correspondingly seeing more new startups seeking financing within our loan portal.

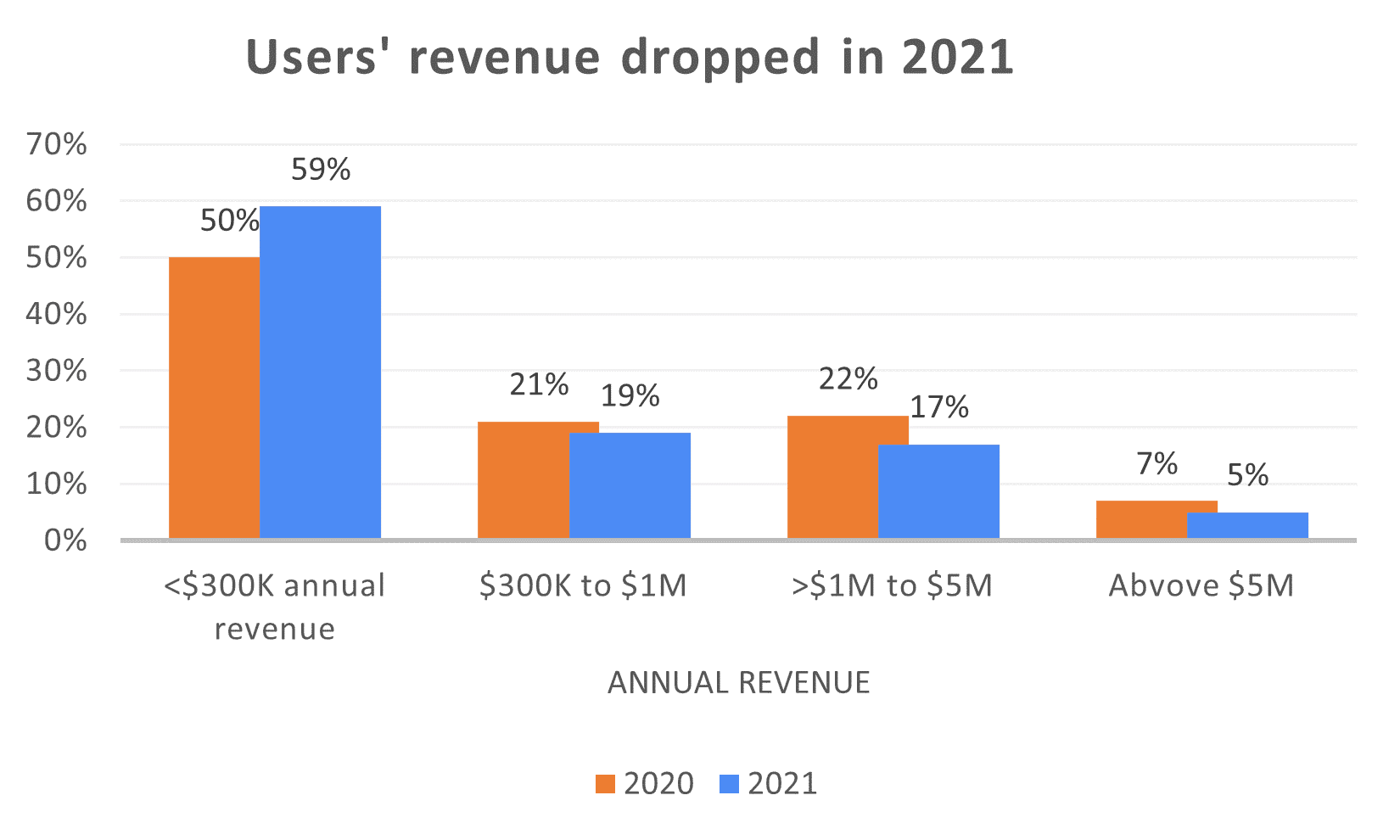

Users’ revenue profile

In 2021, revenue size of our loan comparison portal’s users dropped compared to users in 2020.

Users with the smallest annual revenue size in our survey, below $300K, formed the biggest share of respondents at 59%, versus 50% in 2020’s survey.

Total users who reported higher annual revenue of between $1M to $5M and above $5M formed 22% of users in 2021, a significant drop from 29% in 2020.

This indicates that there were more SMEs with smaller revenue base seeking financing in 2021 vis-à-vis 2020, where we saw bigger SMEs exploring financing within our loan portal.

Profitability of users remain consistent

50% of SME users in 2021 stated that they were profitable in the previous financial year of 2020, during the onset of the pandemic and amid circuit breaker lockdowns imposed in that period.

This is compared to 51% of users in 2020 who indicated profitability in the financial year 2019, pre-Covid.

This could be due to the unprecedented support measures the Singapore Government rolled out to protect jobs and stave off economic scarring in Budget 2020 and subsequent supplementary Budgets.

As a result, the impact on profitability for financial year 2020 remained largely consistent with 2019 amongst our users. However, we note that we have no data on whether profit margins of users were affected.

Although percentage of respondents who were profitable remained consistent over financial year 2020 and 2019, we presumed that overall profit margins and net profit in absolute figures might have dropped in financial year 2020 vs 2019, due to inevitable economic impact of Covid-19.

Breakdown of approved loan quantum

More than half (52%) of SMEs within our platform who secured financing successfully obtained loan amounts between $101K to $300K.

Average SME loan size originated decreased in 2021

Average loan quantum originated within our platform in 2021 is $224,398. This is a decrease of about 28% from 2020’s all-time high average loan quantum of $310,909.

Taken into context with other data points highlighted prior, the decrease in average loan quantum could be attributed to a greater number of smaller sized SMEs seeking financing in 2021.

Whereas in 2020, higher average loan amount raised could be attributed to a consolidated spike in SMEs with stronger credit profile seeking financing earlier on in the pandemic.

On the supply side of the equilibrium, banks and financial institutions might have adjusted their risk appetite in accordance with a decrease in risk sharing of government assisted financing schemes, from 90% in 2020 to 70% in 2021.

We note that although average loan ticket size has dropped in 2021, it is still almost 69% higher than the average loan amount of $132,500 in 2019 pre-Covid. This suggests that credit conditions are still generally accommodative for SMEs in 2021 and there remains an alleviated demand for financing.

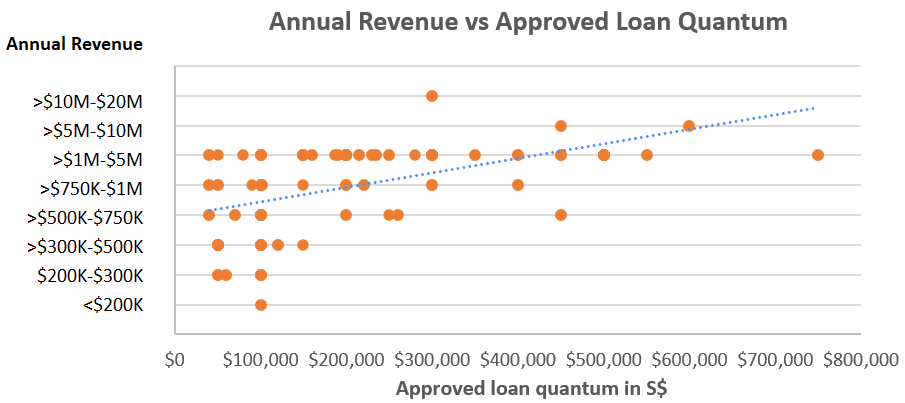

Correlation between annual revenue and approved loan quantum

We extracted a statistically significant sample of our platform’s users who successfully secured financing. Their annual revenue and approved loan quantum were plotted on a graph.

We found that there is a direct correlation between the annual revenue of a borrower and successful approved loan quantum.

In general, SMEs with higher revenue typically qualify for higher financing amounts as compared to their smaller counterparts.

Loan origination across lender types

Data for 2021 indicates an increased share of loan originations for foreign bank within our platform, from 24% in 2020 to 32% in 2021.

We see this as a return to normalcy. In 2020, dominant share of loan originations (73%) within our platform were overwhelmingly underwritten by local banks.

This could be due to knee jerk reaction by SMEs to the uncertainties caused by the pandemic, resulting in a surge of business loan applications back in 2020. Bulk of these applications were submitted to local banks probably due to their brand name familiarity with SMEs.

* ’Others’ financiers within our platform are alternative lenders such as P2P lending platforms, private B2B financiers, alternative lending fintech firms etc.

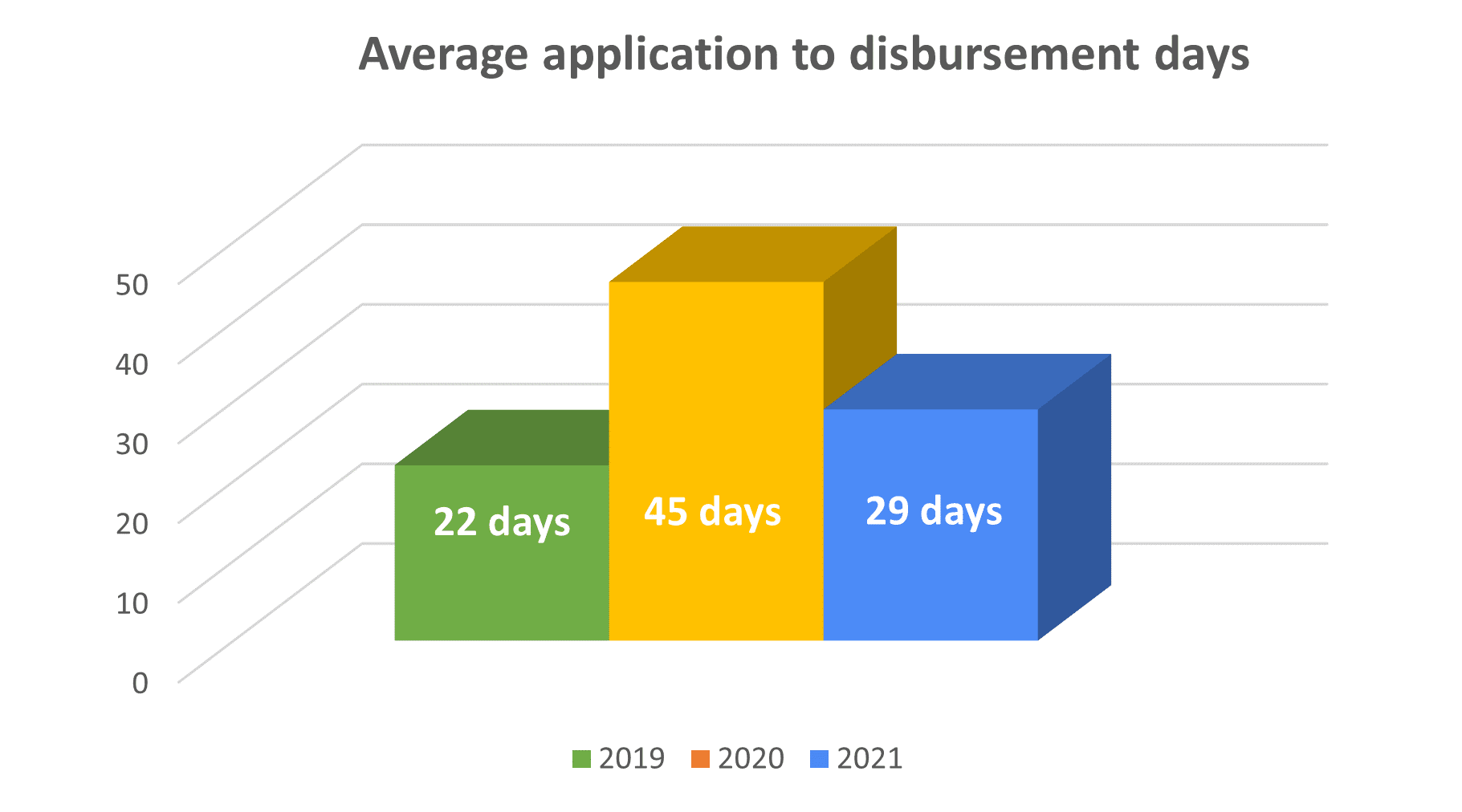

Average application to disbursement turnaround time

The average turnaround time from application to funds disbursement (for approved applications) took 29 days in 2021. This is a marked improvement from 2020’s turnaround time of 45 days.

More bank employees returning to office and familiarity with work-from-home norms could be reasons why applications are processed faster.

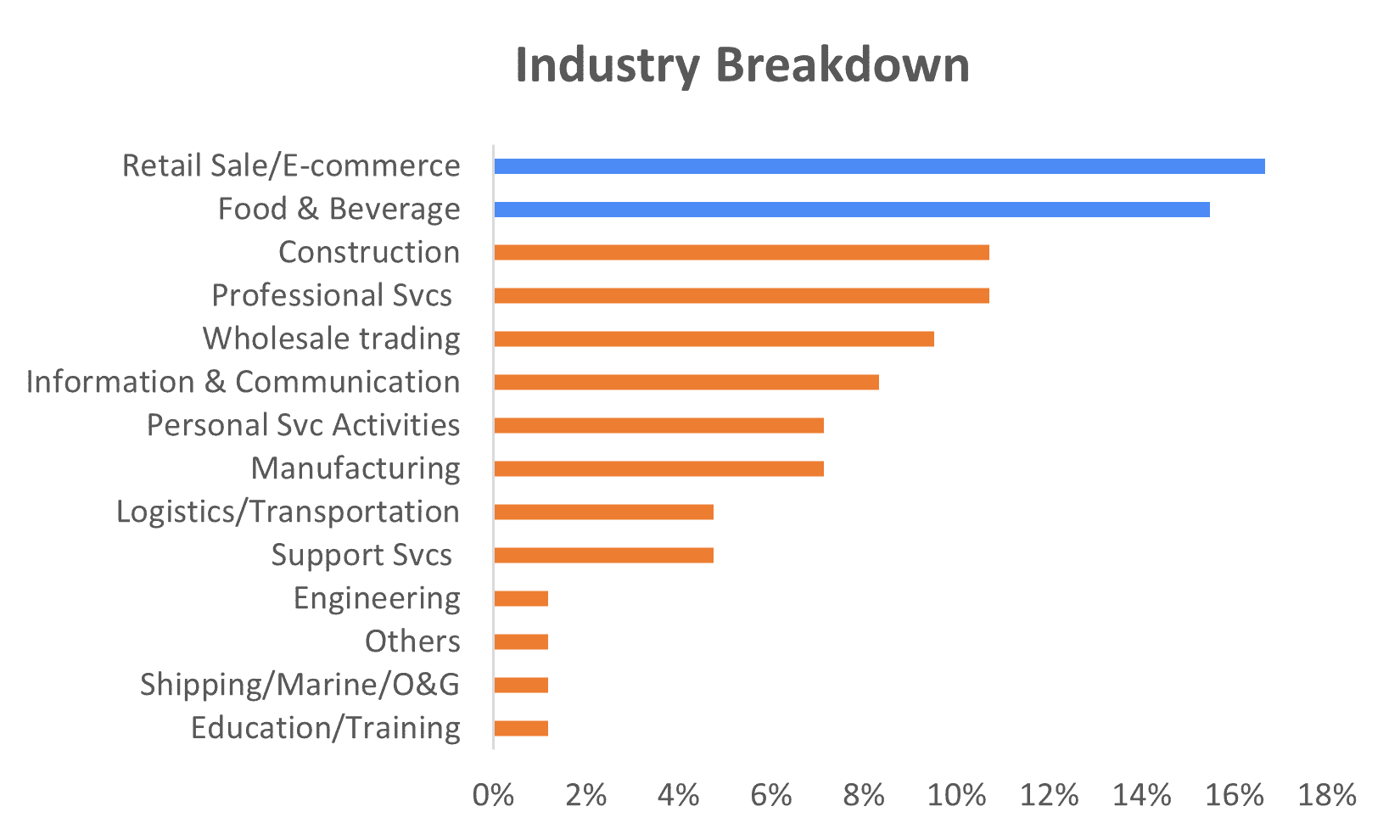

Industry Breakdown

Sectors that formed the highest percentage of SMEs seeking financing via our platform include Retail Sale (17%), Food & Beverage (15%) and Construction (11%).

Not incidentally, SMEs in these three primarily domestic facing industries have been impacted most adversely by Covid-19.

Other industries that were less affected by Covid-19 such as Professional Services (11%), Wholesale Trading/Distribution (10%) and Information & Communication (8%) are also actively seeking financing to scale and expand.

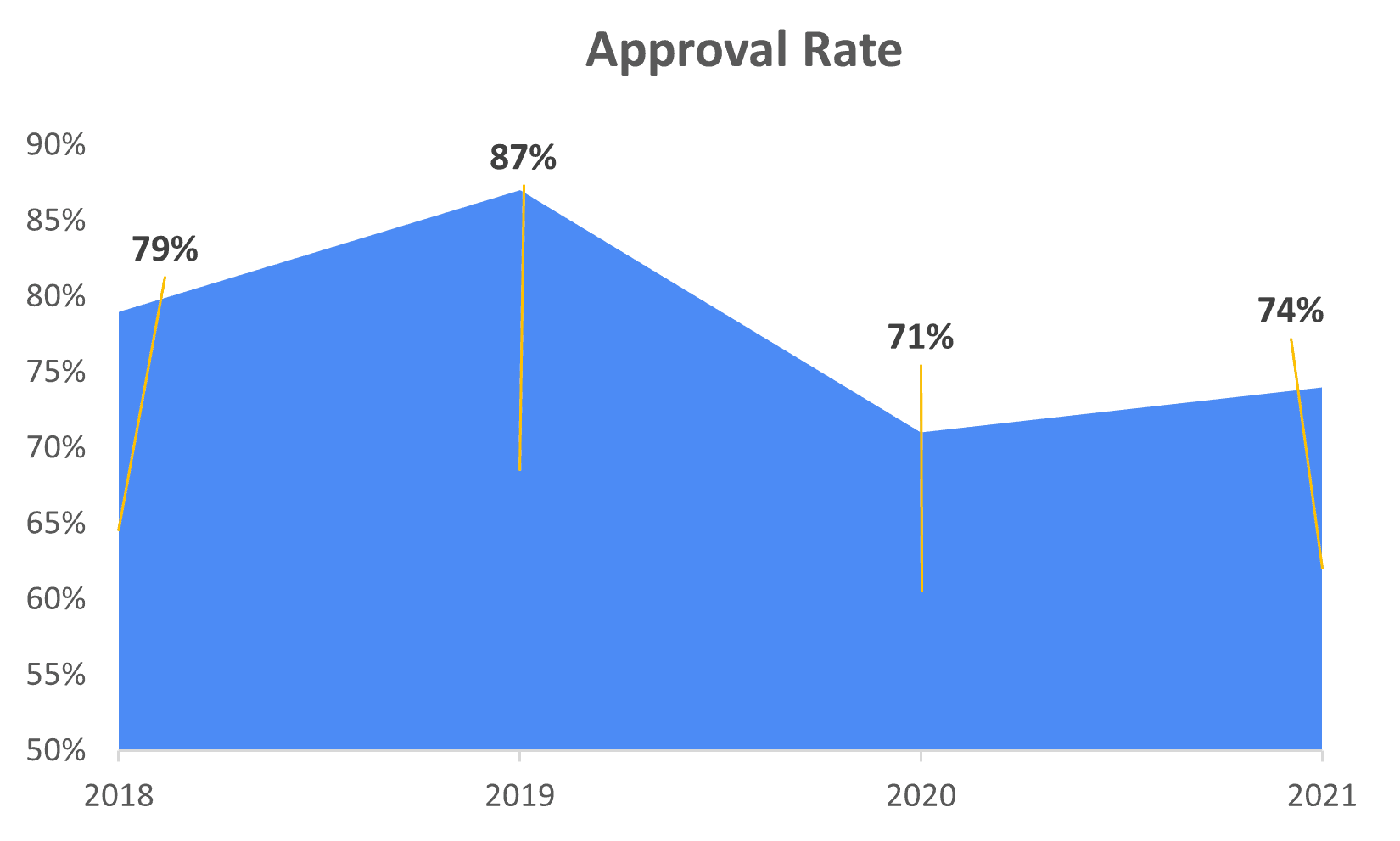

Approval rate improved in 2021

Approval rate for SME loan applications initiated within our platform improved slightly to 74% in 2021, from 71% in 2020.

Generally, credit underwriting is still tight as most lenders have not totally lifted their selective sector specific defensive posture adopted during the height of the pandemic in 2020.

However, credit conditions are considered accommodative with higher than pre-Covid loan quantum approved, and historically low interest rate for borrowers who make the mark.

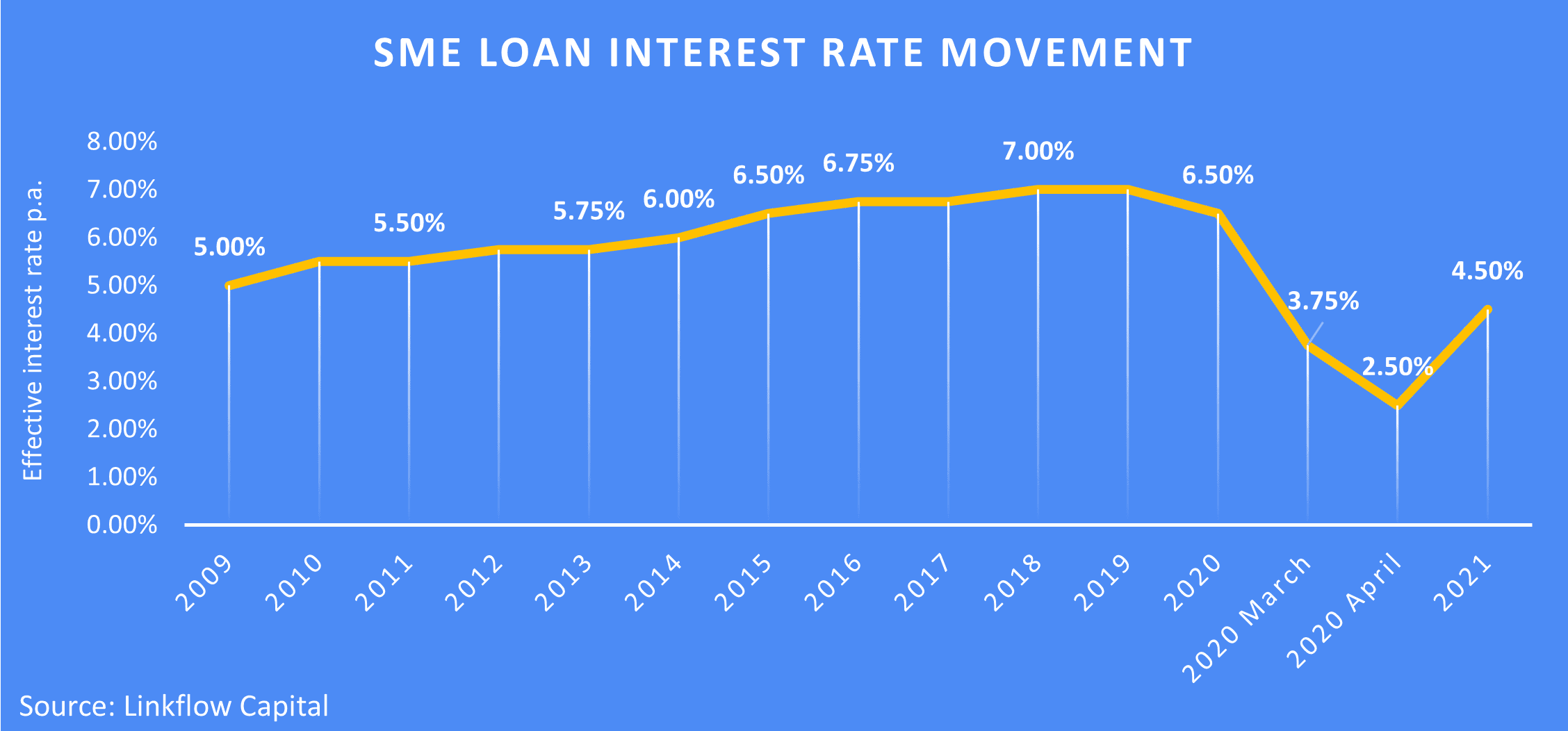

Interest rate movement for SME loans at all-time lows

We track average interest rate movement for SME loans (typically government assisted financing schemes) across last 12 years.

Average SME business loan interest rate sunk to a historical low of 2.5% p.a. in 2020. Rates began moving up in 2021 to average of 4.5% p.a. which is still below previous recorded low of 5% last seen in 2009.

In 2020, borrowing rates for SMEs have been kept low with MAS’s support. A MAS SGD facility [2] to participating financial institutions for government assisted loans helped eligible SMEs gain access to lower cost funding.

In the short to midterm, we are expecting borrowing rates to head north towards second half of 2022 and beyond, due to US Fed rates hikes as well as Singapore’s tepid economic recovery.

Total loans to businesses 2021

According to MAS’s data on total loans to businesses in 2021, business lending has generally been improving on a month-to-month basis.

For both halves of 2021, system wide business lending is on a general upward trend on a month-on-month basis.

As Singapore transitions to an endemic Covid-19 and the gradual normalization of global travel, business recovery is expected to further improve in 2022.

With an expected GDP growth forecast of between 3% to 5% for 2022, [4] we expect overall business lending to continue rising, albeit in a gradual upwards slope due to lingering contingent risks in global major economies.

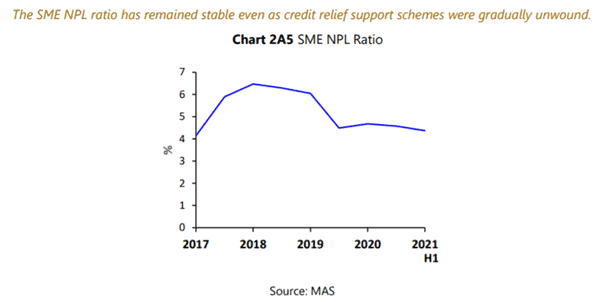

SME NPL (non-performing loans) ratio

The NPL (non-performing loans) ratio for SMEs according to MAS’s Financial Stability Review [5] report was about 4% in 2021.

Notably, NPL ratio for SMEs did not worsen in 2021 and remained consistent with 2020’s NPL ratio, despite various government credit relief support schemes being gradually unwound in 2021.

This could be an indication of the resilience and strength of the recovering economy in 2021, as well as the strong buffers government policies enacted, helping to cushion the worst blows of Covid-19 on SMEs.

Number of SMEs tapping into government financing schemes

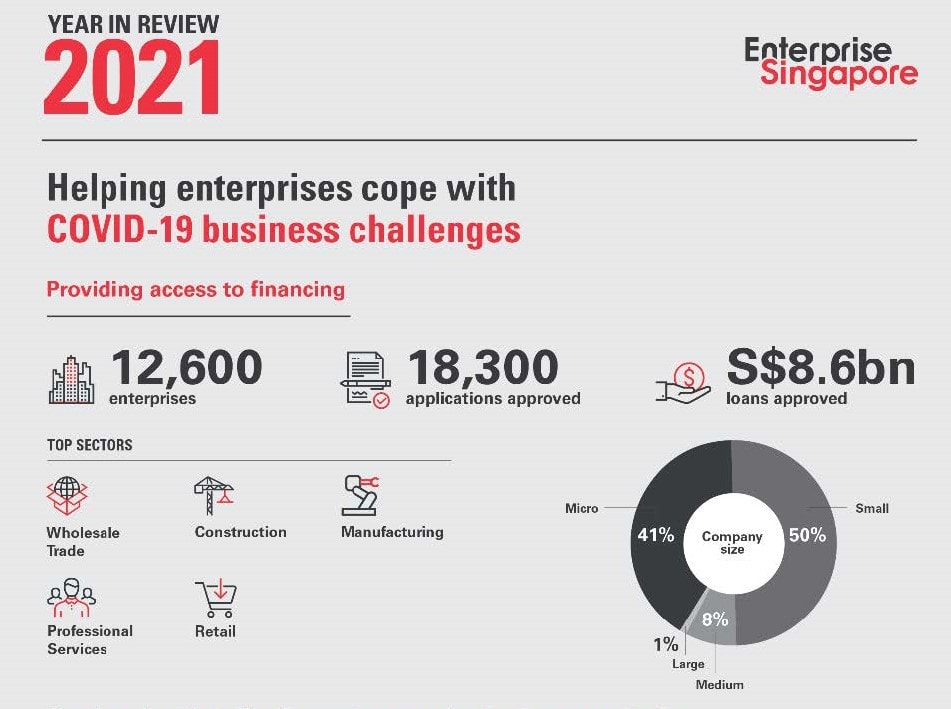

According to Enterprise Singapore’s data in their 2021 Annual Report, total SME loans approved under various government assisted financing schemes dropped to $8.6B in 2021. This is about a 54% drop from $18.6B approved in 2020.

91% of total loans in 2021 went to Micro and Small Enterprises, which are probably the segment of SMEs most vulnerable to external economic shocks due to weaker balance sheet compared to bigger sized peers.

“The amount of loans disbursed in 2021 remained elevated – at four times higher than the pre-pandemic years of 2019 and 2018”, said Mr Png.“That means that there’s still quite a fair number of companies that are still struggling,” he added”

Mr Png Cheong Boon – CEO, Enterprise Singapore

Data source: Enterprise Singapore Annual Reports 2019 to 2021

Observing the data from Enterprise Singapore, the total number of SMEs that tapped onto government assisted loans in 2021 remain high at about 12,600 in 2021, as compared to 7,900 pre-Covid.

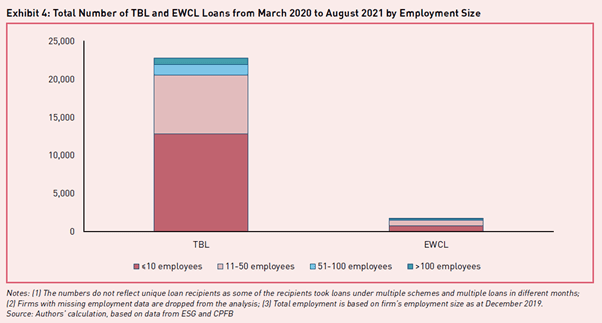

Impact of Temporary Bridging Loan to SMEs during Covid-19

Source: MTI

A study from MTI (Ministry of Trade & Industry) [6] found that most borrowers of the Temporary Bridging Loan (TBL) are SMEs with employment size below 10 employees and between 11 to 50 employees.

The TBL was introduced in Budget 2020 to help SMEs access financing and cope with Covid-19’s impact. Government risk sharing and lower interest rate are key features of the loan. It has been further extended to September 2022.

Together with the data point from Enterprise Singapore where 91% of government assisted loans in 2021 were disbursed to Micro and Small Enterprises, we can conclude that the Temporary Bridging Loan has delivered the most impact to its intended segment of recipients.

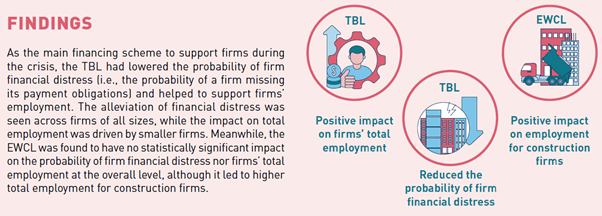

The same study from MTI has also derived that the TBL has lowered the probability of financial distress for SMEs during the pandemic. The TBL also has a positive impact on total employment, especially for smaller firms.

From our take on the ground, we are of the opinion that the TBL, SME Working Capital Loan and government initiated moratorium schemes during the crisis have been critical in stabilizing credit conditions, preventing a sharp spike in NPLs and financial distress for SMEs.

This in turn sustained SMEs in retaining workforce, supported employment, and reduced adverse economic scarring effects.

The close cooperation between authorities and financial institutions in rolling out and implementing the TBL helped serve the immediate needs of SMEs for cash infusions and working capital to tide over the crisis.

There are continued uncertainties in the Covid-19 public health situation and the global economy. The relevant authorities should continue monitor closely credit accessibility conditions, financing costs and receivables delinquency for SMEs, and be swift to extend further liquidity support if the situation warrants.

Forecast and outlook for SME financing landscape 2022

Interest rate is set to go up

The Temporary Bridging Loan has been the main financing scheme introduced to help SMEs access financing for the past 2 years. Cost of financing has been kept low with MAS’s support.

It is scheduled to end on 30 September 2022. Barring any unforeseen external shocks, we do not think the scheme will be further extended, in view of Singapore’s gradual reopening and recovering economic prospects.

As such, we foresee that SME financing interest rates will increase significantly from 4th quarter 2022, in line with the general market interest rate hikes.

SME credit policies

We observed that more banks have been increasingly relying on programme-based lending credit models for the SME lending segment.

Such programmatic lending models apply a uniform simplified and standardized credit criteria for underwriting SME loans. It is easier to originate loans at scale while reducing lenders’ acquisition processing costs.

However, there’s a draw back for SMEs assessed on such pre-qualification assessment systems: Credit criteria become increasingly restrictive and opaque. For applicants who do not fit into a predefined narrow set of credit profile, or fail the mark marginally, there is typically no form of recourse.

Digital banks and alternative lenders

In 2020, MAS announced four successful digital bank applicants, including two digital full banks and two digital wholesale banks.

The introduction of new entrant digital banks will help promote greater financial inclusivity. Digital banks are envisaged to cater for needs of underserved segments such as young micro-enterprises and underbanked SMEs, and to provide alternative competition to mainstream banks.

The digital banks are expected to launch operations in 2022 and we look forward to the fresh impetus these new entrants will bring to the local SME financing landscape.

Summary

2021 was a challenging year for most SMEs to navigate, albeit the recovery theme after the worst of the pandemic.

Swift government policies introduced in 2020 averted SMEs from the brunt of the economic damage caused by Covid-19.

As SMEs in most sectors start to recover gradually, the phased withdrawal of relief support schemes should also provide the impetus for firms to re-think process of strengthening competitiveness and improving productivity amidst evolving structural trends post-pandemic.

There are ample training grants for SMEs to equip and upgrade their workforce with the necessary skillsets to cope with today’s technology and automation trends.

SMEs should also continue to deepen digital capabilities, which in turn will be a catalyst for cost savings, productivity gains and a possible pivot to new growth opportunities.

Linkflow Capital operates a SME loan portal for users to compare their business financing options online instantly. We have been aggregating data collated from our SME financing comparison platform since 2017.…

Linkflow Capital operates a SME loan portal for users to compare their business financing options online instantly. We have been aggregating data collated from our SME financing comparison platform since 2017.…

Linkflow Capital operates a SME loan portal for users to compare their business financing options online instantly. We have been aggregating data collated from our SME financing comparison platform since 2017.…